Everyone has ideas.

Some of these ideas may be decent, while others are probably not so good.

Even if your idea is great, there’s a big difference between having a great idea and creating a successful startup company.

Do you have what it takes to be an entrepreneur?

If your answer is yes, then you need to know how to take an idea and turn it into a startup company.

For those of you who have never started a business before, it can sound like an intimidating task.

Don’t get me wrong – I’m not saying that getting your startup company up and running is an easy mission by any stretch.

It will take hard work, dedication, money, some sleepless nights, and even some failure before you succeed.

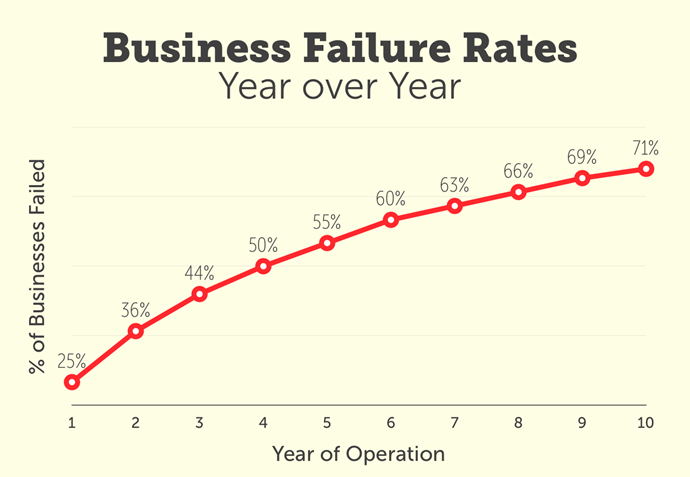

71% of businesses fail within 10 years.

Once you get your company off the ground, you need to work just as hard to keep it going each year.

With that said, it’s helpful to have a guide and a set of instructions to follow that can help you get started.

Fortunately, I’ve created several startup companies like Crazy Egg, Hello Bar, and KISSmetrics.

I’m happy to share my knowledge and experience to help make things a little easier and less stressful for you as you’re going through this process.

While you’ll realistically take hundreds of steps to launch your company, I’ve narrowed down the top 7 steps that you need to take to get your startup off the ground.

We’ll outline and discuss each step in detail so you have a better understanding of what I’m talking about.

You can use this guide as your blueprint for launching your startup company.

1. Make a business plan

Having an idea is one thing, but having a legitimate business plan is another story.

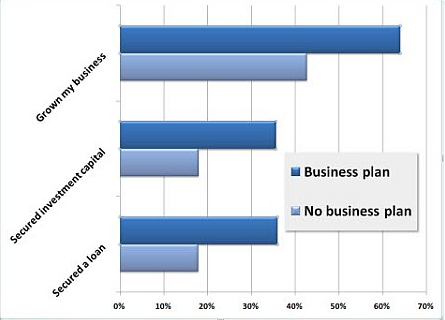

Let’s take a look at these numbers.

Of people who start companies with a completed business plan:

- 36% obtained a loan.

- 36% received investment capital.

- 64% grew their business.

Of the people without a business plan:

- 18% obtained a loan.

- 18% received investment capital.

- 43% grew their business.

We’ll discuss the financial aspects of launching your startup company shortly, but clearly, you need money to start and operate a new business.

A proper business plan gives you a significant advantage.

So how do you make a business plan?

In simple terms, a business plan is the written description of your company’s future.

You outline what you want to do and how you’re planning to do it.

Typically, these plans outline the first 3 to 5 years of your business strategy.

The business plan needs to be the first thing on your list because you’ll use it to help you with some of the remaining steps.

2. Secure appropriate funding

You’ll need adequate capital to get yourself off the ground.

There’s no magic number that applies to all businesses.

The startup costs will obviously vary from industry to industry, so your company may require more or less funding depending on the situation.

For a small, part-time startup with no equipment, employee salaries, or overhead to worry about, it may only cost you less than $10,000.

Other ventures may cost millions.

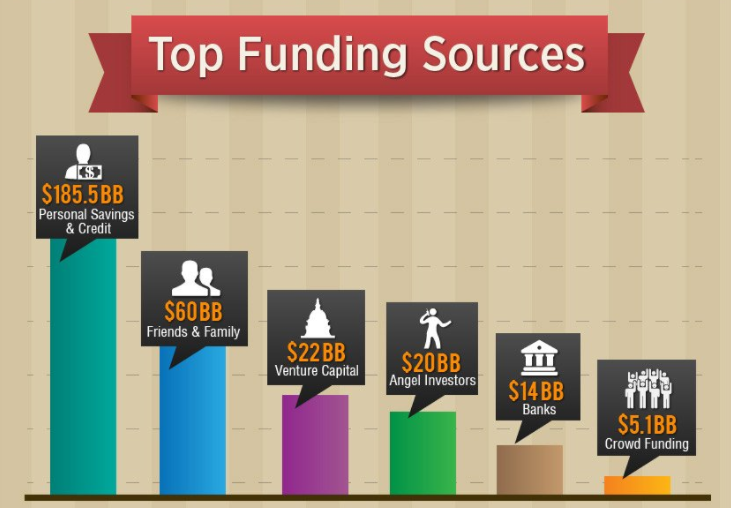

What’s the primary source of this funding?

Roughly 565,000 startup companies launch in the United States every month.

On average, these businesses raise $78,406.

Based on the graphic above, the vast majority of this money comes out of the entrepreneurs’ pockets.

The cost of doing business is much higher than people initially think.

Let’s circle back to our business plan for a minute.

All business plans contain a financial plan. This plan usually includes:

- Balance sheet

- Sales forecast

- Profit and loss statement

- Cash-flow statement

82% of businesses fail due to cash-flow problems.

You’ll use these financial statements to determine how much funding you need to raise in order to get started.

You may discover that the number is significantly higher than you originally anticipated.

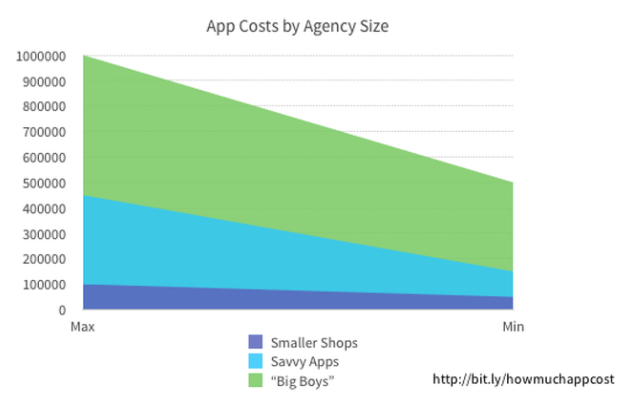

For example, I’m sure you’ve heard someone say, “That would make a great app,” or “I should make an app for this.”

Do you know how much it costs to make a mobile application?

Even if you start a small app shop with only a few people, it’s likely going to cost you anywhere from $50,000 to $100,000.

And that’s just to make it.

It doesn’t include the cost of running it or customer acquisition costs.

The point I’m making is this – in order to secure the appropriate funding, you need to find out how much money you need to raise.

To find this number, you need to research and predict realistic financials in your business plan.

Let’s say you discover that your startup needs $100,000 to get off the ground.

What if you don’t have $100,000?

Don’t worry – your dream isn’t dead yet.

You’ve got some options, but you want to weigh them all cautiously to avoid paying massive interest rates.

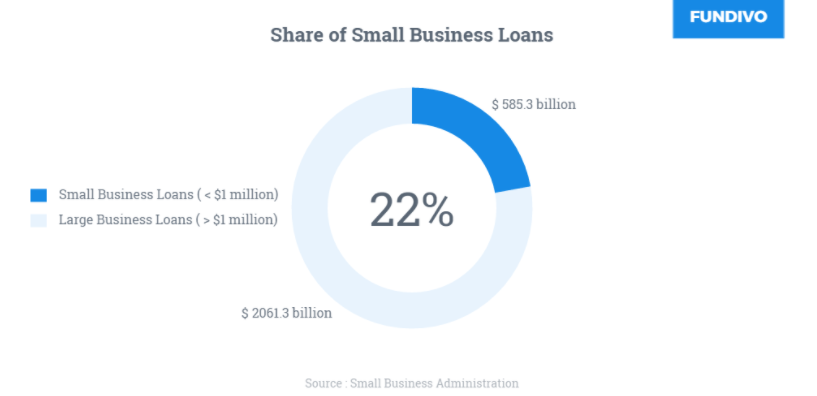

22% of business loans go to small businesses. The vast majority of business loans are for large companies that are already established.

There’s a reason why this number is so low.

Banks are less likely to give large amounts of money to new companies with no income or assets to default on.

That’s why bank funding was second to last on the funding sources graphic that we referenced and discussed earlier.

So if you can’t get money from a bank, or if you can only find a bank that’s offering you an outrageous interest rate, what other options do you have?

Find investors.

Investors can be:

- Friends

- Family

- Angel investors

- Venture capitalists

Proceed carefully because you don’t want to start giving away significant equity in your company before you even get started.

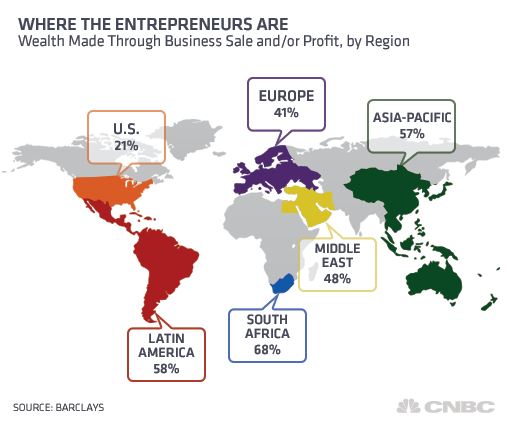

The type of business you’re starting also influences the likelihood that angel investors and venture capitalists will be willing to give you funding.

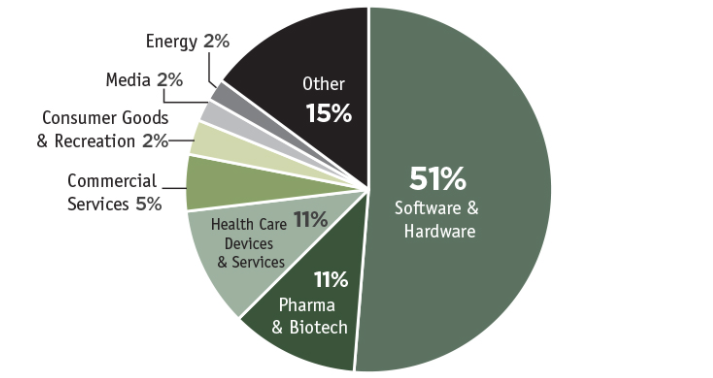

Over half of venture capitalist money in the United States is invested in software and technology.

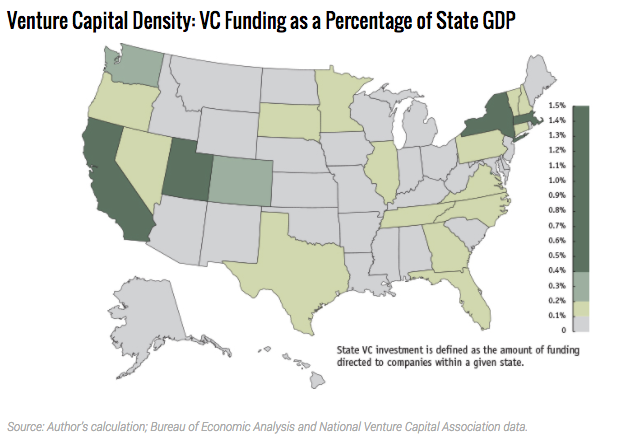

It may not be easy to find venture capitalists if you’re not in a certain area.

What do I mean by this?

This graphic explains how your location can make a difference.

If you find a potential investor, you need to know how to pitch your idea quickly and effectively.

You need to have your financial numbers memorized forwards and backward.

Refer to your business plan.

Make sure it’s presentable so you can give them a copy, but you also need to know how to successfully verbalize your startup strategy.

It’s imperative that your business plan has a proper executive summary.

Investors are busy and may not take the time to read through your entire plan if the executive summary doesn’t give them a reason to move forward.

Once you secure the appropriate funding, you can proceed to the next step of launching your startup company.

3. Surround yourself with the right people

You’re going to need some help while launching your startup company.

So where do you start?

Certain people often get overlooked when entrepreneurs are getting their business started.

Sure, you may realize that you’ll need some staff and a manager to help run your company. Is that it?

How many people do you need?

It depends on the industry.

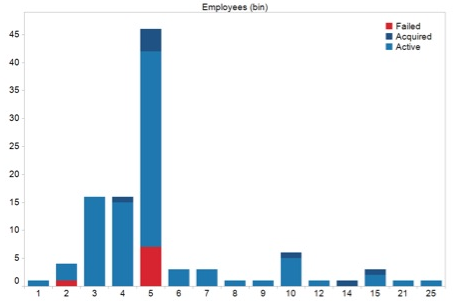

Let’s take a look at an example from a study about the amount of employees for startup companies in the technology industry.

Based on this information, the vast majority of startup companies are small teams.

These numbers would be significantly different if you were starting a business in the restaurant industry.

You would need servers, a kitchen staff, bartenders, and managers.

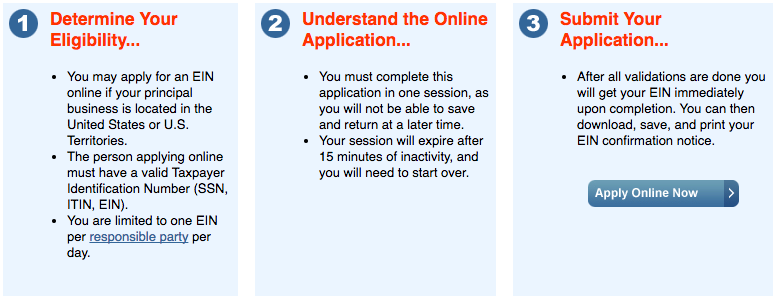

Before you do anything, you need to register your business name.

Once your business gets registered, you’ll need to get a federal tax ID number, as well, from the IRS.

The IRS lets you submit your business information online to get your employer identification number (EIN).

You also need to consult with a:

- Lawyer

- Accountant

- Financial advisor

Unless you’re an expert in law, finances, and accounting, these three people can help save your business some money in the long run.

They can explain the legal requirements and tax obligations based on how you structure your business.

- Sole proprietorship

- Partnership

- Corporation

- Limited liability company

While your lawyer, accountant, and financial advisors are not necessarily employees on your payroll, they are still important people to surround yourself with.

Don’t forget about insurance.

Shop around and find an insurance agent who can get you plenty of coverage at an affordable rate.

Now you can start hiring people within your organization.

4. Find a location and build a website

Your startup company needs a physical address and a web address.

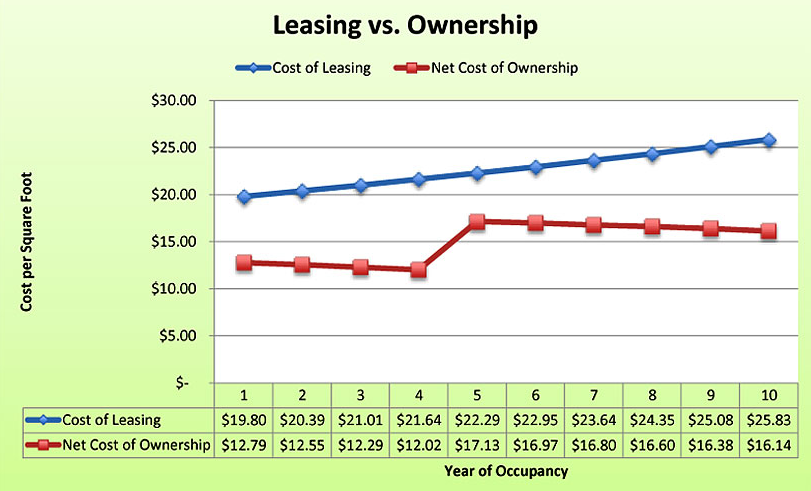

Whether it’s offices, retail space, or a manufacturing location, you need to buy or lease a property to operate your business.

As you can see from the graph, leasing property for your business is significantly more expensive than buying.

With that said, it may not be realistic for all entrepreneurs to tie up the majority of their capital in real estate.

You should strategize for this in your business plan.

Try to secure enough funding so that you can afford to buy property.

It’s worth the investment and will save you money in the long run.

You also need to create a website.

Don’t wait until the day your business officially launches to get your website off the ground.

It’s never too early to start promoting your business.

If customers are searching online for a service in your industry, you want them to know that you exist, even if you’re not quite open for business yet.

You can even start generating some income through your website.

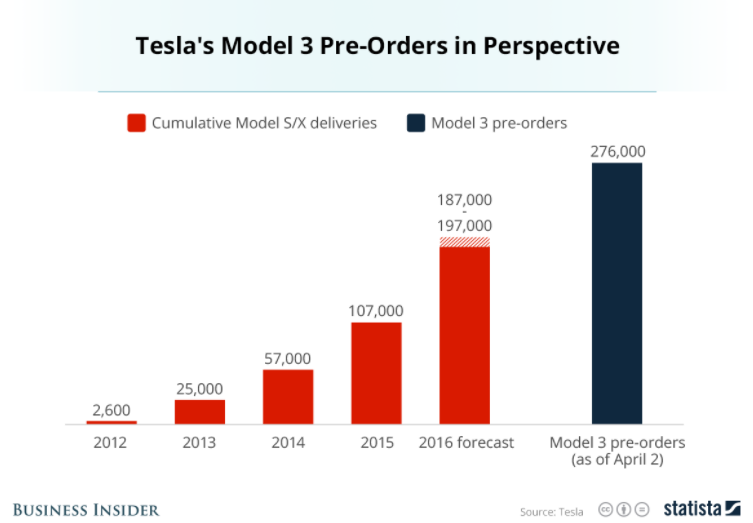

If it’s applicable, start taking some pre-orders and scheduling appointments.

For those of you who aren’t convinced on the pre-orders business model, take notes from Tesla.

Just make sure that your website is fast.

I can’t stress this point enough.

I’ve got a video tutorial that explains how to speed up your website.

Today, your company can’t survive without an online presence.

If you’ve never launched a website before, you can follow my guide to building your first website.

It may sound like a tough task, but it’s really not that difficult.

Once your website is up and running, you need to expand your digital presence.

Utilize social media platforms like:

- Snapchat

Your prospective customers are using these platforms, so you need to be on them, as well.

5. Become a marketing expert

If you’re not a marketing expert, you need to become one.

You might have the best product or service in the world, but if nobody knows about it, then your startup can’t succeed.

Learn how to use digital marketing techniques like:

- Content marketing

- Affiliate marketing

- Email marketing

- Search engine optimization (SEO)

- Social media marketing (SMM)

- Search engine marketing (SEM)

- Pay-per-click advertising (PPC)

If you’re starting a small business in a local community, you can take advantage of some older and conventional methods such as:

- Print advertising

- Radio advertisements

- Television

- Billboards

While these methods can be productive, outbound marketing efforts are not as effective as they used to be.

If you’re stuck in an old-school mindset and can’t adapt to the new trends from the marketing world, you’ll struggle to get your startup off the ground.

For those of you who aren’t efficient marketers, there is no shame in hiring a marketing director or even a marketing team, depending on the size of your company.

Your marketing efforts will be one of the most important, if not the most important, components of launching your startup business.

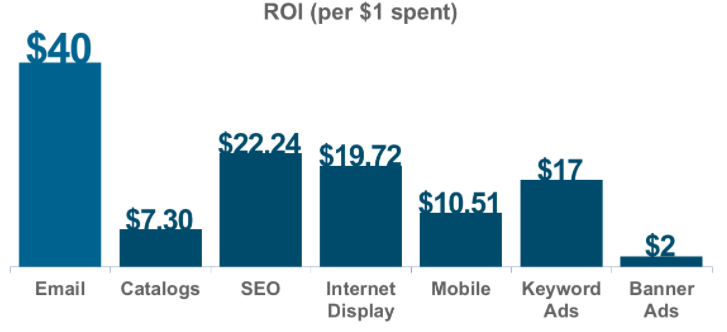

Allocate a marketing budget.

Determine how you’re going to distribute this money across different channels.

Have a plan and try to maximize your return on investment for each campaign.

The graph displays where companies are having the highest and lowest ROI based on their marketing costs.

Take these numbers into consideration before you spend your entire budget on something like banner ads.

The bottom line is this: Marketing needs to be a top priority for your startup company.

6. Build a customer base

If you’re following this plan in order, the good news is that you’re already on the right track to building a customer base.

Starting a website, growing your digital presence, and becoming an effective marketer are all steps in the right direction.

But now it’s time to put these efforts to the test.

Open your doors (or website) for business.

Getting a customer to make a purchase is the first step.

But this isn’t nearly enough.

You need to keep your customers coming back.

This statement holds true for physical store locations as well as e-commerce businesses.

So what’s the key to getting repeat customers?

It’s no secret.

- Customer service

- Customer service

- Customer service

The customer needs to be your main priority. They are the lifelines of your business, and they need to be treated accordingly.

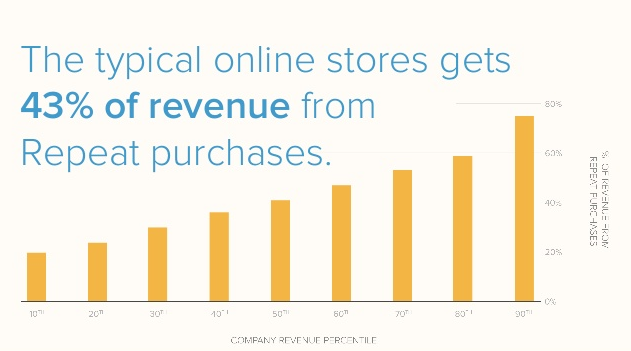

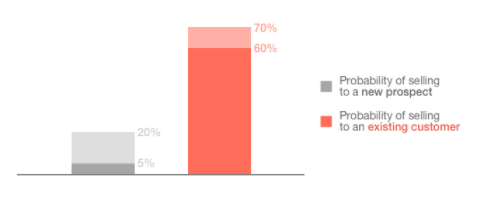

Once you establish a steady customer base, you can use it to your advantage.

You’ll get more money from your existing customers than from new ones.

How do you sell more products or services to your current customers?

It’s a more effective method than cross selling.

Less than 0.5% of customers respond to cross selling.

Over 4% of your customers will buy an upsell.

These strategies both double back to having effective marketing campaigns.

Overall, establishing, building, and maintaining a customer base will help you get your startup company off the ground.

7. Prepare for anything

Expect the unexpected.

Launching your startup company won’t be easy, and you need to plan for some hurdles along the way.

Don’t let these speed bumps become roadblocks.

You can’t get discouraged when something goes wrong.

Preserve and push through it.

The difficulties that you’ll face while launching your startup company will help prepare you for the tough road ahead.

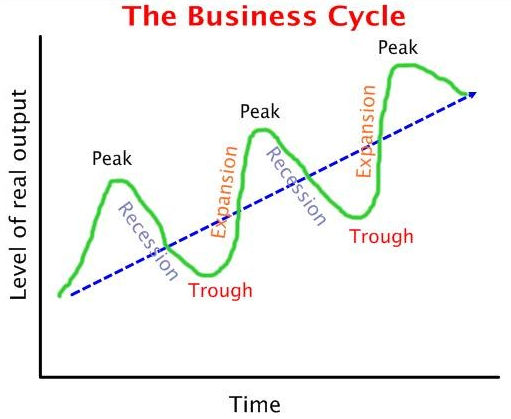

Even after your business is up and running, it won’t necessarily be smooth sailing for the entire lifecycle of your company.

You will face peaks and valleys while your company operates.

Mistakes and setbacks happen.

Some of these things will be out of your control, like a natural disaster or a crisis with the nation’s economy.

Employees will come and go.

You’ll face tough decisions and crossroads.

Sometimes, you’ll even make the wrong decision.

That’s OK.

Part of being an entrepreneur is learning from your mistakes.

It’s important to recognize when you’ve done something wrong, move forward, and try your best to make sure it doesn’t happen again.

Pay your bills.

Pay your taxes.

Operate within the confines of the law.

As long as you’re doing these things, you’ll be able to fight through any obstacle your startup company faces in the future.

Conclusion

Let’s recap.

Launching a startup company is not easy.

First, you need to determine if your idea is worth turning into a business.

You also need to decide if you have what it takes to be an entrepreneur.

Even though the United States has over 27 million entrepreneurs, they are still behind other regions of the world.

Why?

Again – it’s not easy.

With that said, having a proper guideline to follow will help simplify the process for you.

Based on what we’ve discussed, you can get your startup off the ground in just 7 steps.

Start by creating a comprehensive business plan.

Your business plan will help you with the remaining steps required to launch your company.

You’ll also need to raise money.

Without proper financial planning, your startup doesn’t stand a chance.

Surround yourself with the right people.

Find people to help you in spaces that are not your strongest areas of expertise.

Don’t forget about lawyers, insurance agents, and accountants.

Build your website and find a physical location for your business operations.

Even if your startup hasn’t launched yet, it’s never too early to start marketing.

These steps will help you build a customer base.

Establishing a steady clientele will grow your startup.

Launching your startup business won’t be perfect, and you need to prepare for unforeseen circumstances.

Proper planning and execution will help limit these hurdles.

How will you raise funding to get your startup company off the ground?

Comments (60)