Founding and running a startup is hard.

I’ve started over 5 companies in the past decade or so and been a partner in others. It’s an incredibly difficult process.

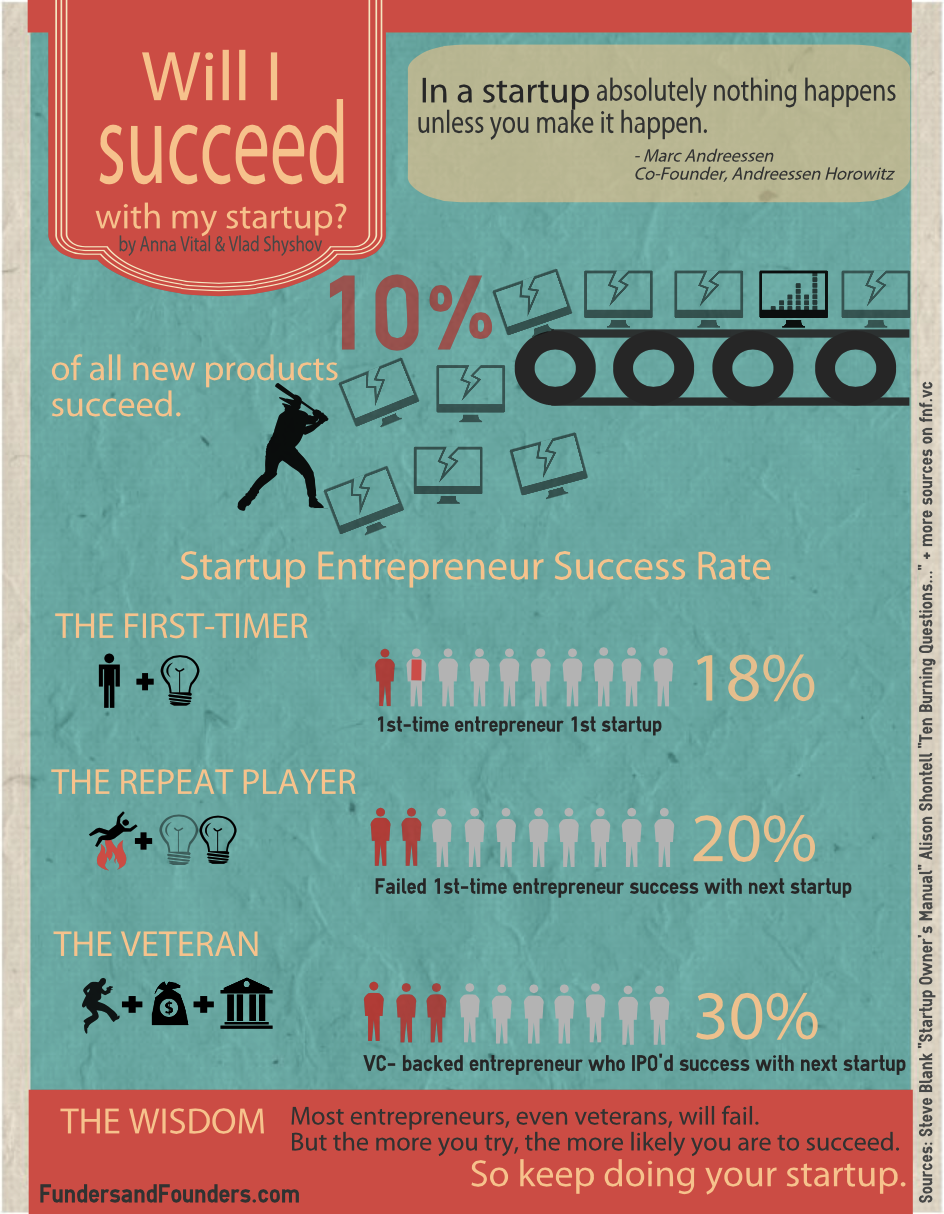

I don’t need to tell you the stats by now. You’ve probably already heard them everywhere.

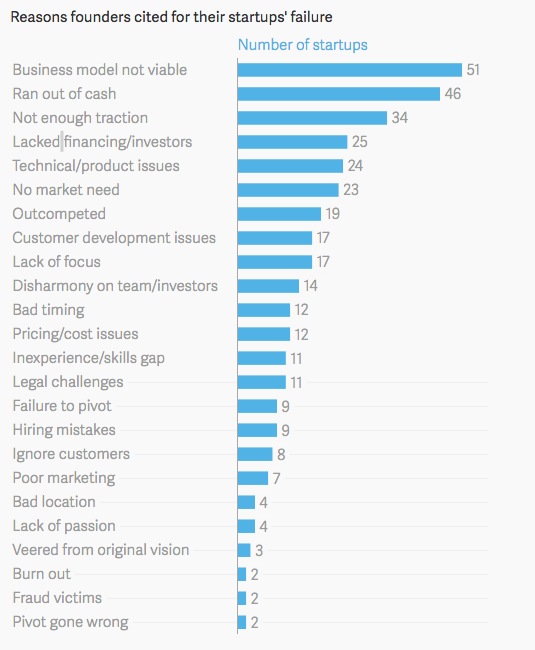

9 out of 10 startups won’t make it past the 5-year mark.

Surviving for the long haul depends on many factors, like your ability to raise funding and attract top talent.

Your experience plays a part, too.

Experienced entrepreneurs are 3x more likely to succeed with a new startup than an inexperienced founder.

That makes sense. The more practice you have at a task, the better you tend to perform.

I would argue there’s a fair bit of luck mixed in, too.

But you can help improve your odds of being one of the long-term survivors, even if you’re working on your first startup.

Below are some of the biggest and most common mistakes startups make. Don’t make the same ones!

Stop hiring the wrong people

When your startup is new, it’s absolutely essential that you hire people who will help you grow.

You can’t afford to waste time paying people who aren’t effective.

That doesn’t mean they’re bad people or bad employees. The wrong hire could still be a talented and committed person.

It just means they’re not the right fit for your startup at that moment.

When you’re scaling up beyond yourself, or beyond you and your co-founders, you need to hire people who match your passion for growth.

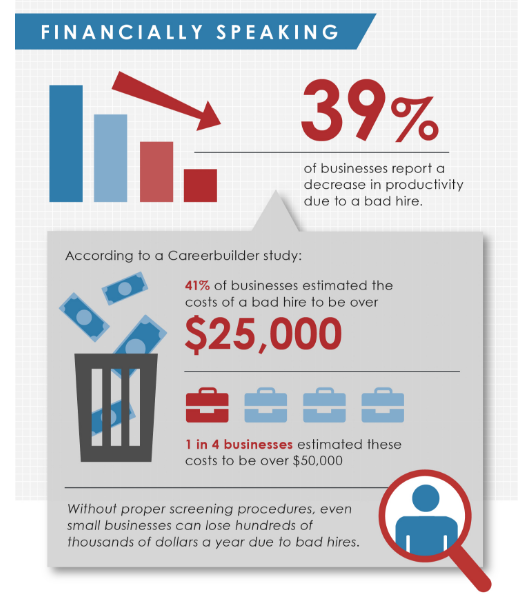

Hiring the wrong person could actually reduce your productivity and cost you up to $50,000.

So how do you make sure you’re hiring the right person?

It starts with the interview.

Top experts say you shouldn’t hire people who only demonstrate strong technical skills. You should be looking for problem-solvers.

Of course, they need to have solid technical skills, too.

However, it’s more important that they can think fast to solve tough problems. This is what will help your startup grow in the early stages.

Thomas Edison had a creative way of testing candidates’ problem-solving abilities before hiring them.

He asked them to eat a bowl of soup.

He would wait to see if they added salt or pepper to the soup before tasting it. If they did, they were out.

Adding salt or pepper before tasting it told Edison that the candidate made assumptions. They assumed the soup wouldn’t be to their liking.

Edison wanted open-minded thinkers. People who weren’t afraid to try the soup first to check for a problem before jumping in with a solution that may not be needed.

The early days of running your startup are similar to Edison’s research: you need problem-solvers.

Ask behavioral interview questions to assess how well each candidate solves problems.

Behavioral questions focus on past events. An example could be, “Tell me about a time you faced a challenge at work and how you overcame it.”

If they can’t think of an example, be like Edison and rule them out.

Stop having processes for everything

You don’t need to have documented procedures for everything.

Processes are important and good to have, but like everything else, they should be used in moderation.

The above image lists some examples of common office time-wasters, like interruptions, waiting for approvals, and data re-entry.

It adds up to a lot of wasted time.

It’s not that processes are evil. It’s just that they can stifle creativity.

Startups need employees who aren’t afraid to think outside the box.

Creative problem-solving can save your startup from financial ruin.

Don’t burden your employees with complicated processes that distract them from doing the work they need to do.

So how many processes should you have?

You need processes. It’s not the Wild West.

The trick is to continually be evolving those processes.

A process can be anything. It’s how your customers get billed. It’s how your team handles a new feature request or bug report.

You also need smart people and creative solutions.

Most of all, you need freedom for those smart people to create creative solutions even if they don’t fit into a nicely-defined checklist.

Encourage your employees to come to you with their suggestions to make current processes more efficient or useful.

Instead of doing away with processes entirely, focus on continually improving them.

Continuous improvement is exactly what it sounds like: always improving your operations to be better, faster, and more productive.

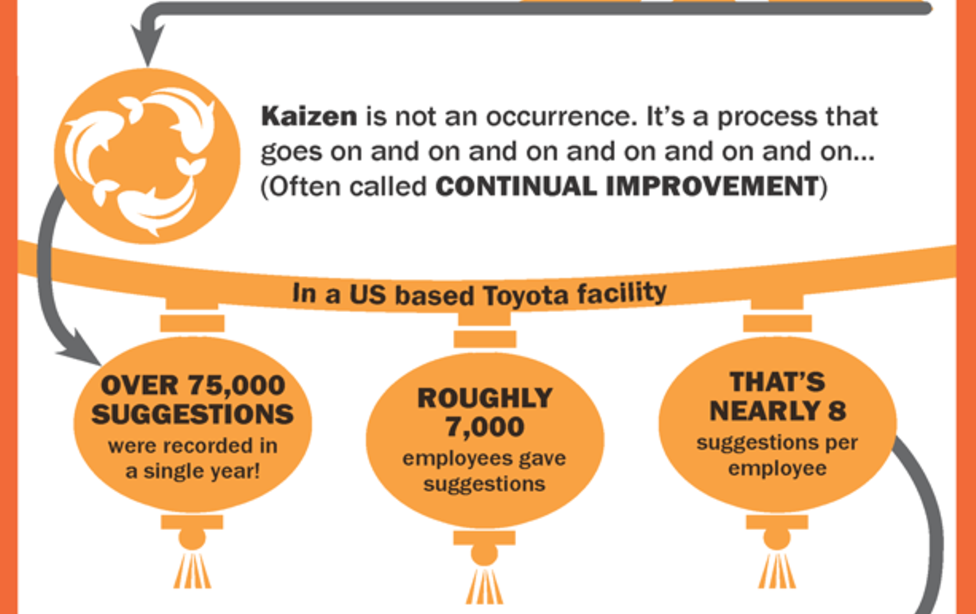

It’s also called the Kaizen method.

Toyota uses the process to improve their manufacturing.

In one plant in the United States, each employee contributed on average 8 new ideas to improve processes.

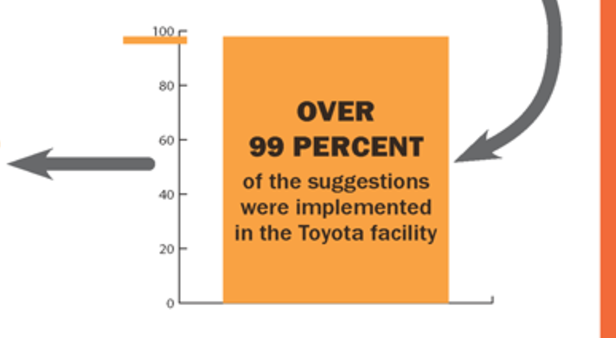

Even more surprisingly, over 99% of the employees’ ideas were implemented by management.

Imagine if you could make that many improvements in just one year!

Focus on solving problems first, then figure out a way to work that solution into your processes for next time.

Stop assuming that you know your customer

I’m going to ask you a question.

When was the last time you held a focus group?

Or even sent out a survey to your customers?

Maybe even talked to one of them?

If you’re not sure of the last time any of these things happened, you’ve got a major problem.

You need to listen to your customers.

The best way is to straight-out ask people for feedback.

You could set up a focus group for your new product idea or a beta test group for your software.

Your beta testers could receive your product for free in exchange for using it. They then would provide suggestions and feedback on features or find bugs.

If you’re just starting out, you’ll need to do a lot of research to determine if your idea has a place in the market.

One online tool I love for that is Answer the Public.

You can type in a keyword and see all the questions real people have searched online for that topic.

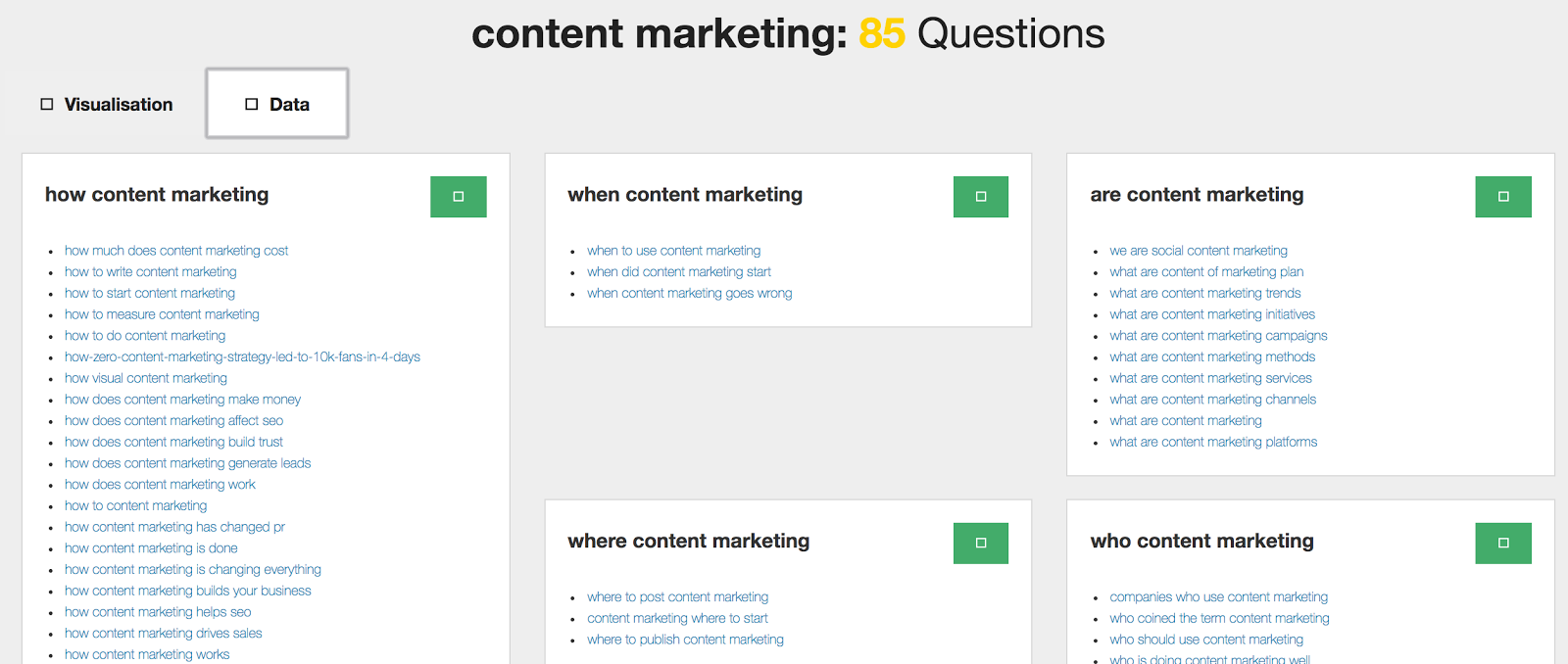

For example, I typed in “content marketing” and I get the results below.

The questions are sorted by who, what, when, where, and why. They also include questions that start with “are.”

This is an easy way to find out the problems people are having or things they want to know more about.

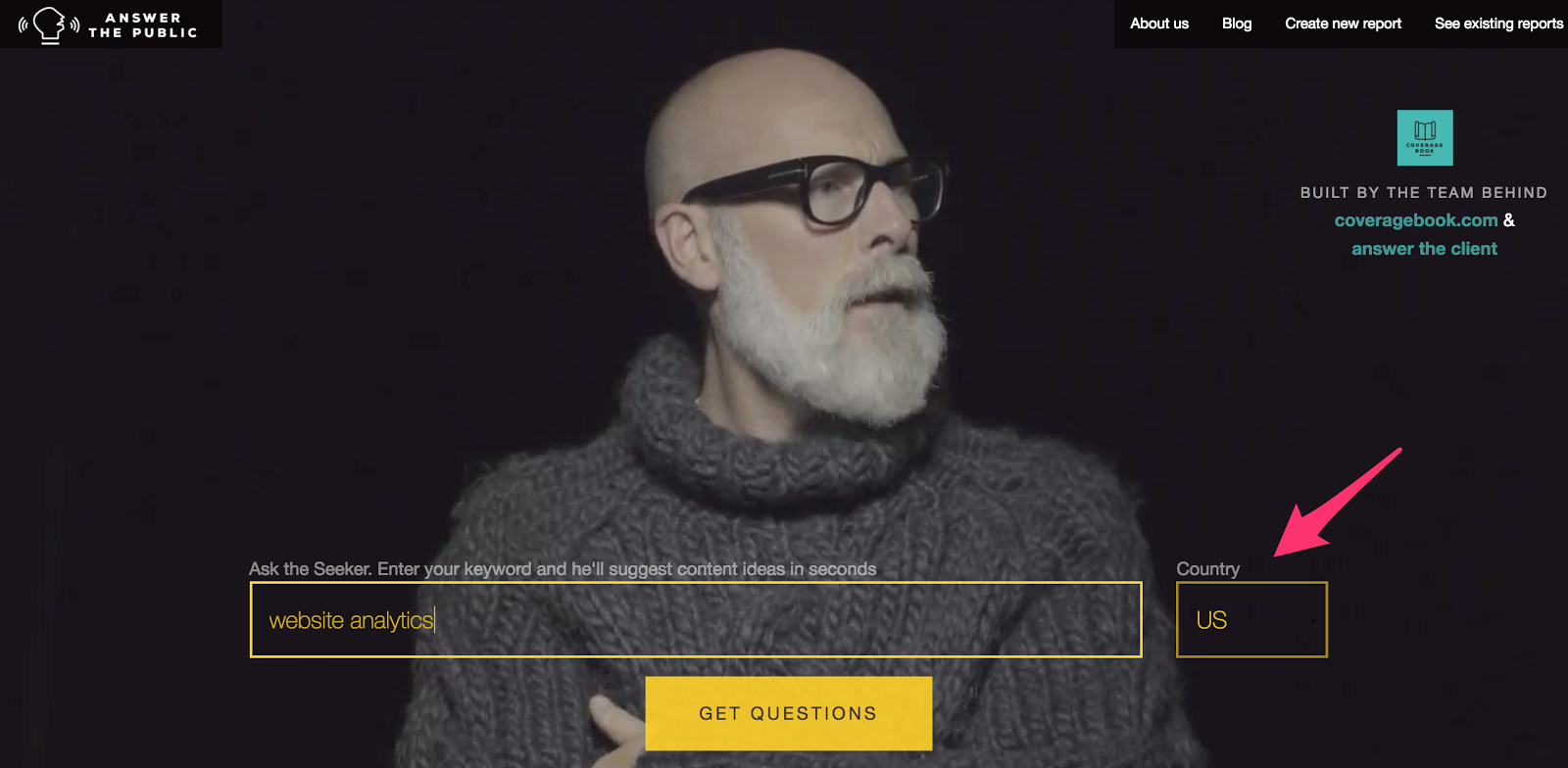

To try it out, go to Answer the Public.

Make sure your country is set to the U.S. (or wherever you live) and type in your keyword. Click on the Get Questions button.

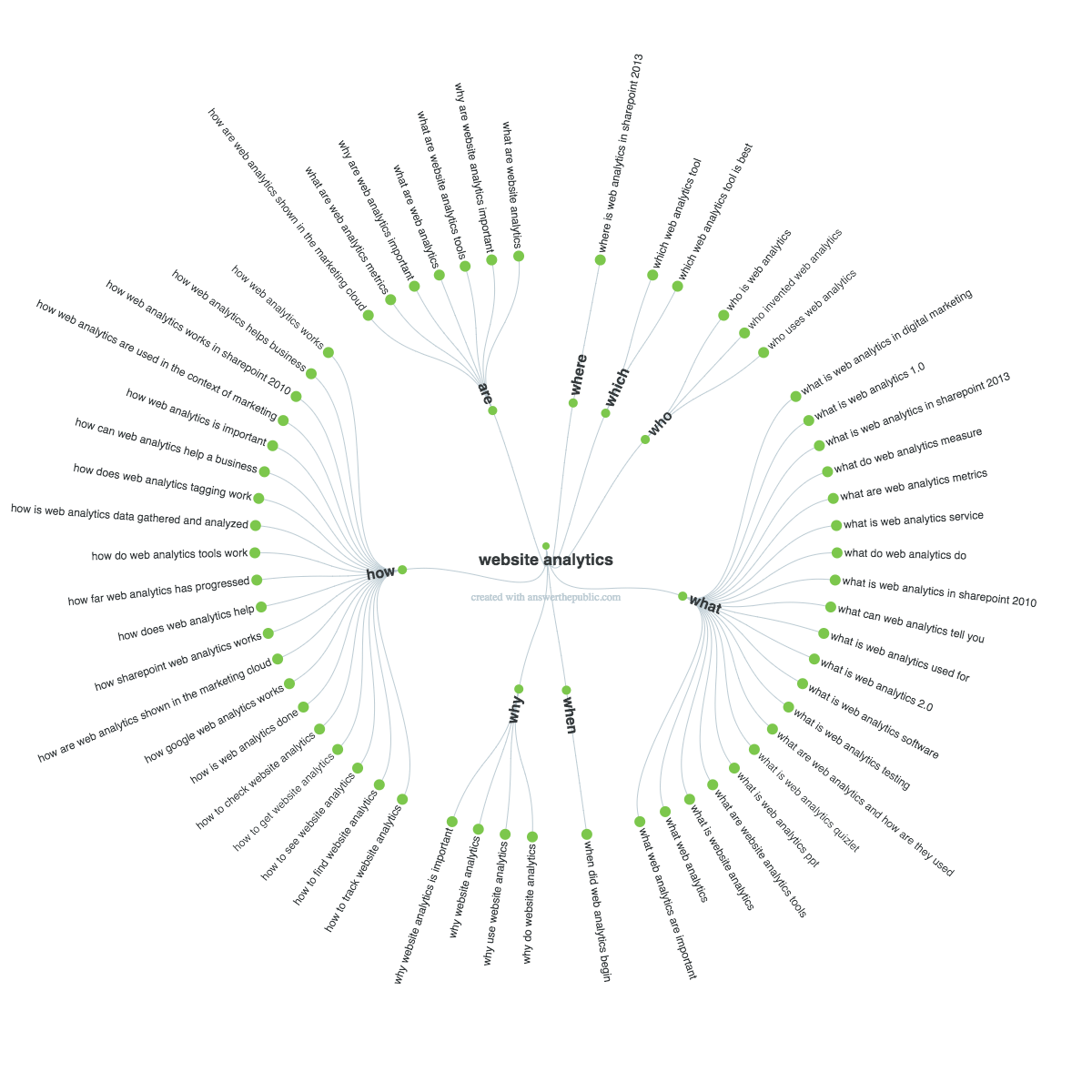

You’ll see the list of questions in a visual diagram first, sorted by who, what, where, etc.

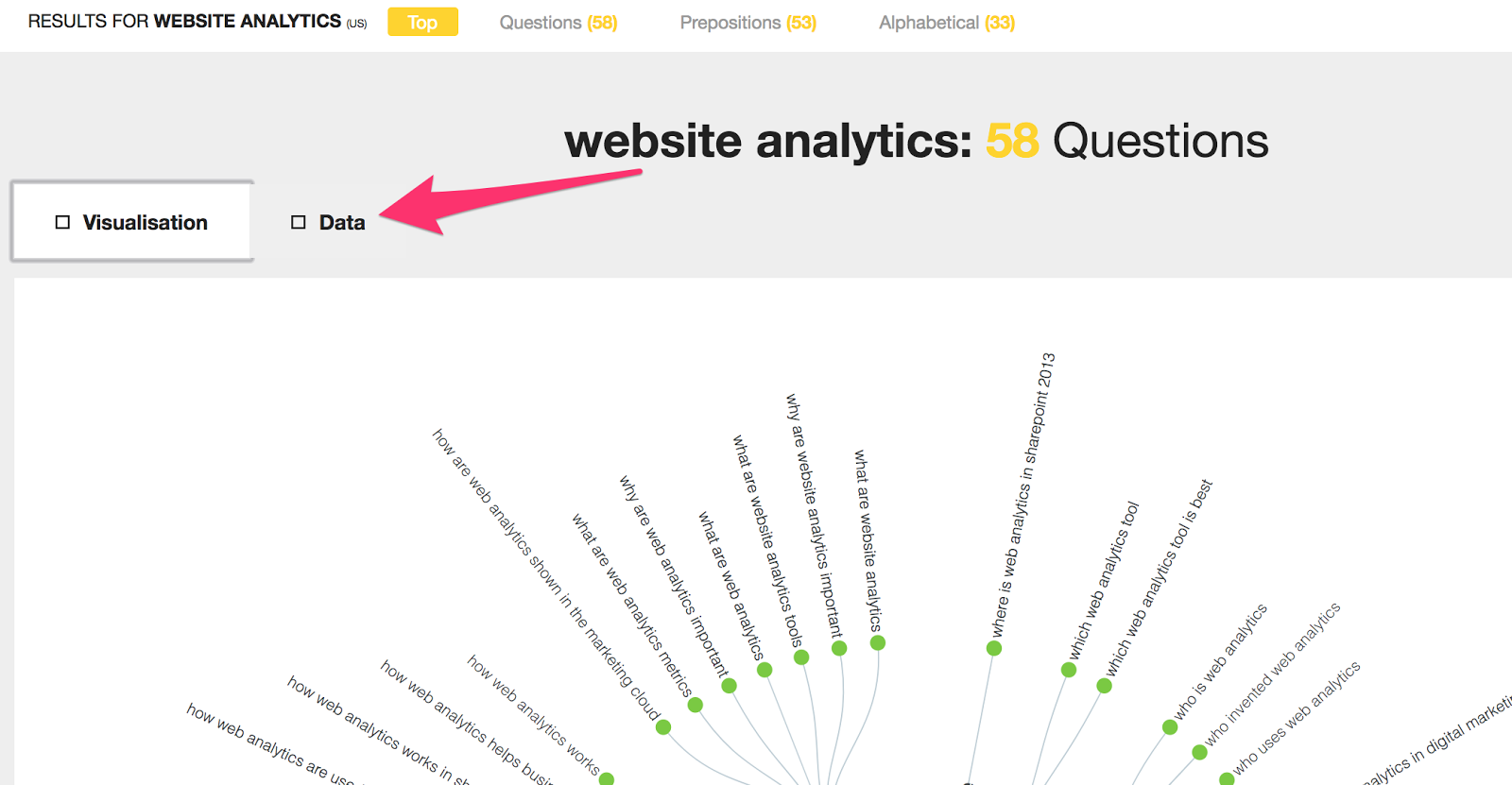

If you prefer to view the questions in a list like the first screenshot I shared, click on Data at the top of the results page.

You will need to do more research than simply a few online search queries.

You should talk to the real humans who you want to attract and figure out what they like and dislike in products like yours.

Don’t assume you know what features your ideal customers want.

Take the time to do research and routinely check in with your customers. It will pay off!

Don’t try to serve everyone

Just as big of a mistake as assuming you know what your customers want is trying to be everything to everyone.

Your target market is not “everyone.”

It should be a small segment of people who have a specific problem that your product solves.

For Crazy Egg, those people are website owners who want to see what’s working on their website and continually optimize it for conversions.

Crazy Egg isn’t for people who only want to know how many people visited their website or where they came from. Google Analytics tells you that for free.

Once you know who your product is for, marketing to them becomes easier.

You don’t just need to know what problem they’re having. You need to know everything about your target market.

Where do they live? Where do they hang out online? What’s most important to them in a product: time-saving, price, certain features?

You need to be able to answer those questions before you start marketing.

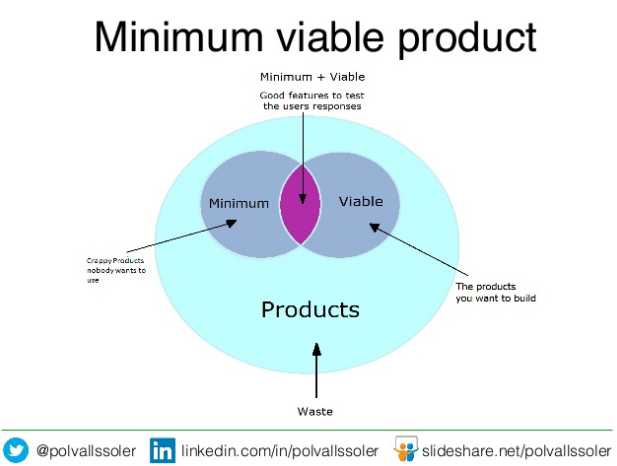

One strategy to make sure your product is a good fit for your target market is to build what’s called a “minimum viable product.” Then test it out with a small group of customers.

Minimum doesn’t mean crappy. Nobody wants to use a crappy product.

You need to build something that still delivers value, but that doesn’t have any extra features or “bells and whistles” yet.

It should have a clean, simple design, even if it’s not the final design interface you want.

Think of it like a prototype of your idea.

It should be functional and offer something new to the customer. Let them test it out, then use their feedback to refine your product in future versions.

That feedback can also provide valuable testimonials you can and should use in your marketing materials.

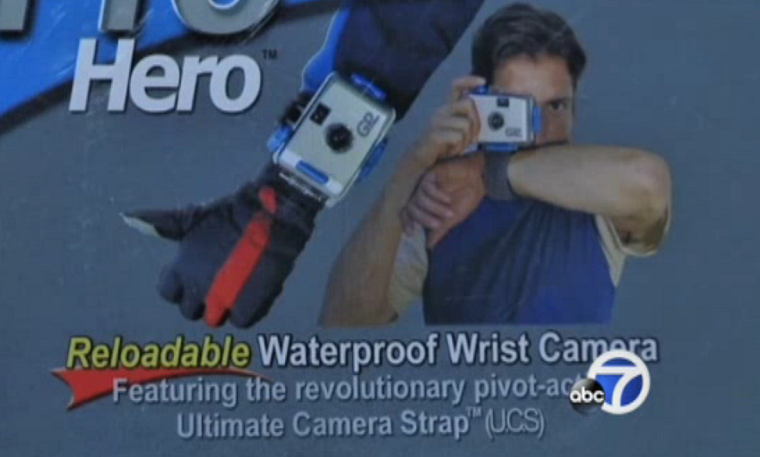

A good example of creating a minimum viable product is how GoPro cameras were invented.

Nick Woodman, who started GoPro in 2004, noticed surfers buying cheap, disposable cameras to take out on the water with them.

At that time, sports videos were filmed either far away (from a boat) or from land. You couldn’t see the action up close.

Nick noticed the surfers taking these cameras out with them to capture the action up close. Because the disposable cameras were cheap, the surfers didn’t mind if they got ruined by the waves.

He decided to make a wrist-mounted 35mm camera that was fully waterproof.

Its hands-free capabilities would be perfect for athletes who wanted to capture the action without having to hold a camera.

He sold the first model on QVC in 2005. It was basically just a camera strapped to your wrist.

The sales of that product proved there was a demand for it.

Nick later created the GoPro models we know now: rugged, digital, and able to record high-definition video. He also created accessories like chest and helmet mounts.

GoPro’s valuation peaked in 2012 at over $2.25 billion.

While 2016 was a tough year for the company, their cameras are still used by action-sports enthusiasts and professionals around the world.

Stop having unnecessary meetings

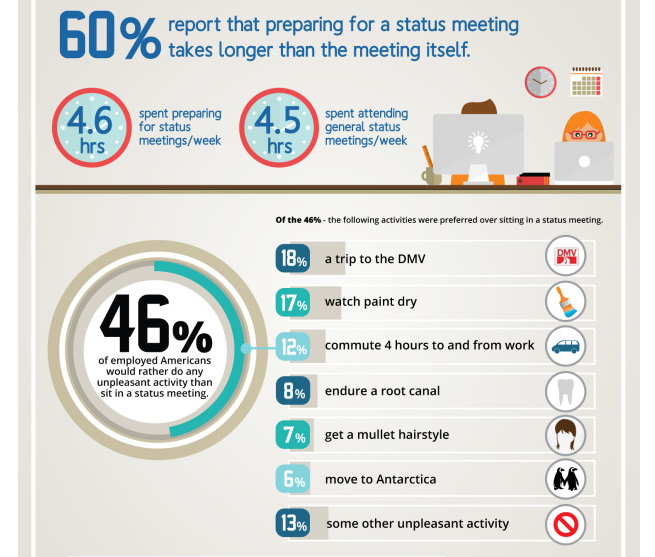

Meetings are a huge cause of lost productivity.

A 2015 study by Clarizen found that 46% of employees would rather do something else than sit in a meeting. Some of the things they said they would rather do included having a root canal, watching paint dry, or even getting a mullet.

They’re not just bad because people don’t want to be there.

Most employees spend longer preparing for a meeting than actually attending the meeting!

This doesn’t mean you should get rid of all meetings.

A popular way to keep everyone informed and manage projects is to hold daily stand-up meetings.

These are also known as “scrum meetings” or “huddles.” They come from the Agile project management philosophy and are commonly seen in software companies.

Daily stand-ups are done, as you might expect, standing up. This helps keep them short.

A stand-up should only take 10-15 minutes. It’s meant as a way for all employees to briefly state what they’re working on and whether they need any help from other teammates.

Stand-ups help everyone stay focused on the overall company goals.

They also help everyone feel like they’re connected to the team, especially if their jobs are done mostly alone.

Don’t waste money on things you don’t need

This one applies to everyone — not just startups!

You don’t need a big, fancy, downtown office with a foosball table. You really don’t.

Don’t give into the hype and compare yourself to other startups that have luxurious offices and perks like free lunches for staff.

Those things are great to offer when you can financially afford to, but offering them too soon could spell the end for your startup.

Remember: 46% of all failed startups flopped because they ran out of money.

It’s not only free food and office space that can derail your budget.

Hiring too many people too soon is a mistake that can drain your bank account.

You may think that if you hire more people than you can afford, they’ll build your product faster, which will allow you to attract paying customers faster.

This is a huge risk.

Hiten and I thought we were going to make much more revenue at first with Crazy Egg than we actually did.

We got rid of our free plan, expecting that more people would sign up for premium paid plans.

That didn’t work out like we planned.

Our first few months of revenue were only a few thousand dollars. Definitely not enough to support a team of employees!

Of course, Crazy Egg went on to become successful, but my point is that you don’t know what your revenues are going to be at first.

Don’t hire a large team thinking it will result in an equally large return on investment.

Stop pitching if it’s not working

If you’re trying to raise capital for your startup, make sure your pitch is effective.

If you’re not receiving any interest from investors, stop using the same pitch. Change your pitch deck or the way you’re presenting your product.

It’s also important to ensure you have a solid elevator pitch.

Ask someone you know to listen to your pitch. Make sure they don’t have any previous knowledge of your company or product.

At the end, they should have a clear idea of what your product does and how it’s different than your competition.

If they don’t, go back to the drawing board and create a new pitch.

Repeat this process until it starts working!

Like product development, you need to be tweaking your messaging and marketing often, too.

There’s no definite answer, but experts say your pitch success rate should be around 15%.

If you’re not reaching that, keep tweaking until you do.

Some common reasons pitches fail are taking too long, not being engaging enough, and getting too hung up on the details.

You don’t want to take longer than 20 minutes to pitch your startup. Consider that a rule!

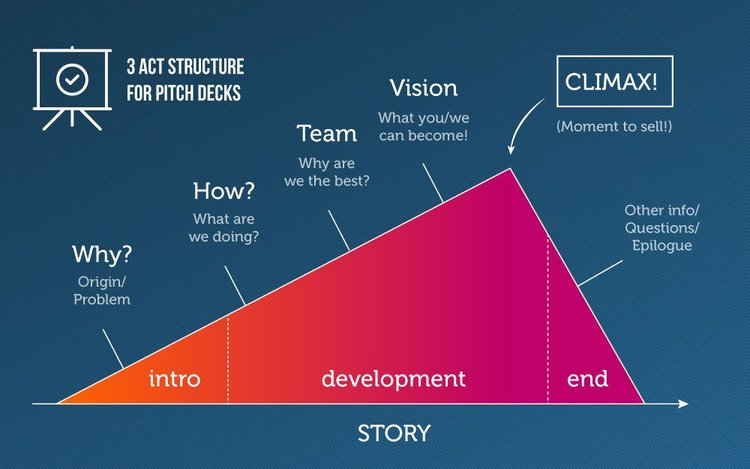

As far as being engaging, make sure you’re telling a story when you’re up there in front of a room full of investors.

Think of it like a movie.

Start off with your introduction. This is why your team created the product.

Then talk about how you created it and the competency of the team behind it.

That all leads into your overall vision.

It could be something like, “To be the best website analytics and user experience testing tool on the market. Crazy Egg is easy to use and provides actionable insights for optimizing your conversion rate.”

Don’t get so into things that you talk about all the nitty gritty aspects, though.

Keep your pitch to the 5,000-foot view of your company. Investors don’t need to know the finer details, like what exact features will be in the next release.

You can always share more details if they ask questions or in follow-up meetings.

You should provide enough detail so investors know the key facts about your product and business model, but not so much that they forget what your vision is.

That’s the point of your pitch: to sell them on your vision.

Conclusion

When you’re starting out, it’s hard to know what to put the most focus on.

You want to get to market quickly so other people don’t beat you, but rushing to market too fast can backfire, too.

Wastage in your company can come in the form of time, tasks, or money. Make sure you’re staying on top of all three to maximize your startup’s chance of success.

It’s crucial to first focus on creating your minimum viable product. Act on user feedback to test and refine it before launching to the public.

Before you can even create your product, you need to know who it’s for.

Who is your ideal customer?

You also need to guard your time.

Don’t waste time on meetings that aren’t important. It’s much more efficient to hire a good team and let them have responsibility for their own areas instead of holding frequent progress meetings.

Building your team is essential to scaling up your startup.

Being frugal also has it advantages. You’ll rely less on investor funding and have more control over your product and company.

Don’t waste money on big offices or expensive perks until your revenue can support it.

The average investor is putting in 200-300% more funding than what’s really required to run a startup!

Give yourself the best chance to succeed by hiring quality talent, launching your minimum viable product, and staying on top of your finances.

Have you run a startup before? If you could go back in time, what would you have done differently in the beginning?

Comments (0)