You know the old expression, “Pull yourself up by your bootstraps?”

It applies to your startup, too.

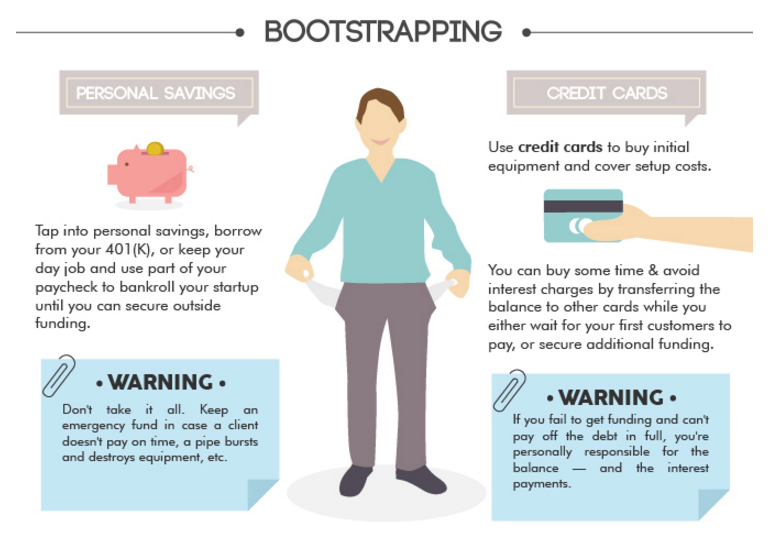

Bootstrapping your startup means growing your business with little or no venture capital or outside investment. It means relying on your own savings and revenue to operate and expand.

It’s not easy to do, but it’s incredibly rewarding.

When Hiten and I started Crazy Egg, we thought we could get funding right away.

We were wrong.

Hiten and I ended up bootstrapping Crazy Egg ourselves to the tune of about $500,000 before we ever got a funding deal.

We pitched to over 30 venture capitalists who all said no.

We eventually received a buyout offer of $6 million, but we didn’t take it.

Looking back, I wish we had. But we were young and idealistic and thought we could do better.

We grew Crazy Egg into a profitable business, but it took many years.

However, using what we learned about bootstrapping ourselves, we were able to raise $10 million in venture funding for KISSmetrics, our second company.

But when KISSmetrics came out, a bootstrapped startup called MixPanel was able to out-market us. That’s when I really noticed the importance of being able to respond quickly to change.

Today I’m going to share some valuable lessons we learned while bootstrapping Crazy Egg and KISSmetrics that you can apply to your own startup.

Let’s dive in.

Sell services first

If you have a great idea for an app, but you aren’t a developer, you need a creative way of raising money to produce your idea.

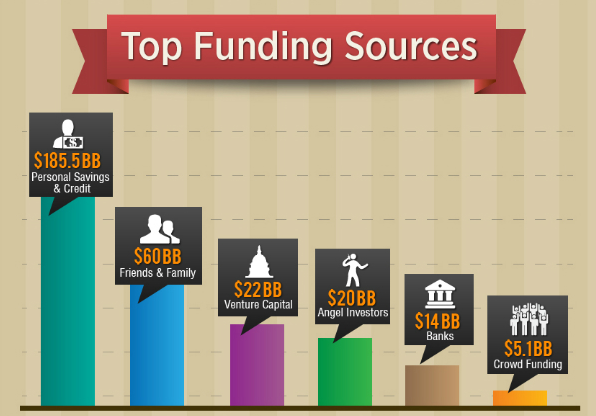

According to Fundable, the majority of startups are bootstrapped. In other words, they’re funded by the founder or co-founders.

A relatively easy way to do this is to sell your consulting or freelance services first.

I say “relatively easy” because it’s still not easy!

But it’s possible.

Jon Westernberg the founder of Creatomic, is on track to make $20,000 per month with his agency. This is because he started selling writing services first.

He knew he needed to earn $3,000 per month to start the development of his marketing platform.

He created a sub-brand of his business targeted to one vertical (real estate) and cold-pitched real estate agents on his email writing service.

Out of 500 pitches, he received 63 replies, which turned into 8 customers.

That got him to the $3,000-per-month mark he wanted. He re-invested all the profit from that into building his agency.

That’s a bootstrapped startup!

I did the same thing when I was starting out. I was able to reinvest the money I earned through SEO consulting into my business.

Even though my first startup failed, I learned valuable lessons that helped the next ones succeed.

I highly urge anyone who’s interested in founding a startup raise funds themselves by selling consulting or freelance services.

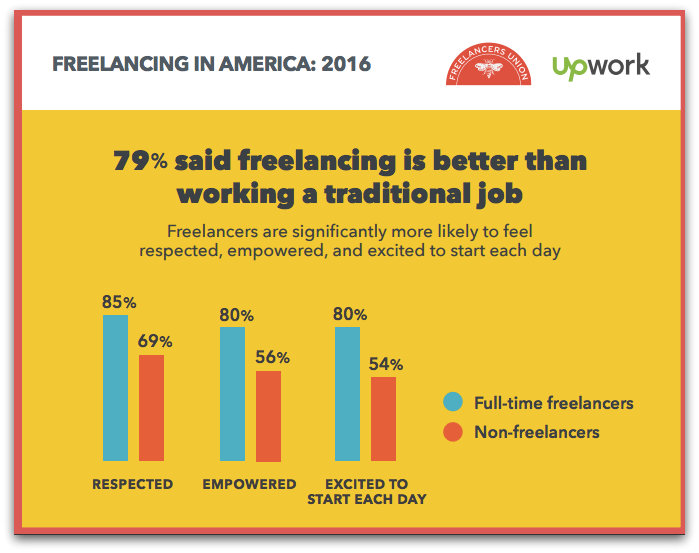

It’s estimated that 35% of America’s current workforce are freelancers.

79% of those freelancers said they’re more satisfied working for themselves than at a traditional job.

Freelancing is on the rise. By 2020, experts say that up to half of the American workforce could be freelancers.

Popular freelance careers are in graphic design, web development, writing, and IT consulting. Don’t let that limit you if you don’t fall into one of those.

As long as you market your services well, you can be successful at freelancing.

Choose a good co-founder

If you’re starting your business with a co-founder, make sure their skill set is complementary to yours.

I don’t mean that they should have the same skills as you!

Hiten and I have founded multiple companies together, most notably Crazy Egg and KISSmetrics. We each handle different aspects of them, which works out well.

Hiten handles all the management, team building, and product development.

I handle sales and marketing.

We didn’t define our roles clearly at first. As time went on and our team grew, I realized I wasn’t good at managing employees.

Hiten gladly took that on, and he’s much better at it.

A good pair of co-founders work well together, and each brings something unique to the table.

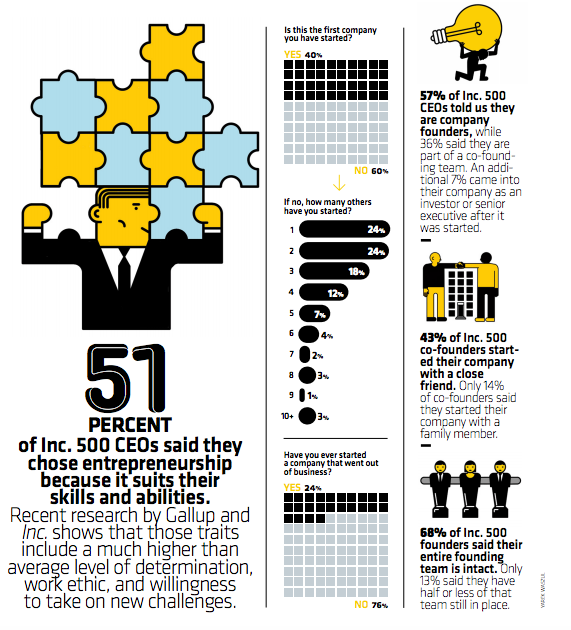

In a 2015 study of Inc. CEOs, 68% said that their team of founding partners remained working at their startups.

Interestingly, 43% of the survey respondents said that they founded their company with a close friend.

This was certainly true for Hiten and I, but I had no idea that it was such a prevalent practice.

Trust is a big part of a successful co-founder relationship.

You have to know the other person is as committed as you are about growing the company and being successful.

You’ll both likely be working long hours for little pay at first.

And if you fail, you don’t want that to disrupt your friendship, but it could happen.

Starting a business with a friend can be a great idea if each of you are 100% committed to making it work.

Think of it like dating.

Starting a business means that you could be tied together for life, so make sure your co-founder is someone you could stand being legally attached to!

If you don’t have any close friends who would make suitable co-founders, you can search for one on sites like Co-Founders Lab.

Co-Founders Lab allows you to search for potential co-founders, advisors, freelancers, and other key team members using their platform.

Seek help from advisors

Even if you and your co-founder have different skill sets, it’s unlikely that both of you will know everything about how to run a company.

Advisors can help your startup grow, but there’s a downside, too.

Most advisors will want a stake in your company in exchange for their help and advice.

After the first round of funding completed for KISSmetrics, Hiten and I signed a bunch of advisors to help us.

We thought they’d help us grow quickly. They did, but the problem was how we structured the deals.

We gave away a lot of equity and diluted our options pool. This limited how much we were able to grow KISSmetrics in the future.

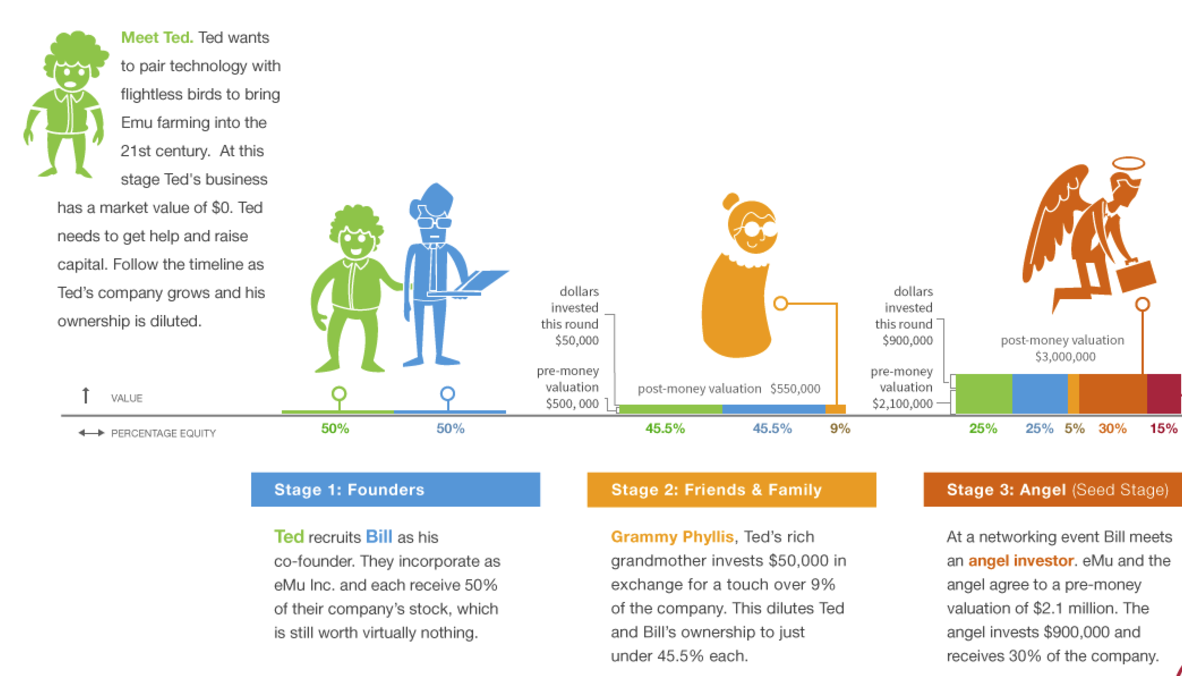

This graphic shows how a founder’s equity gets diluted over time.

You start with half and half, which quickly gets sliced up like pieces of a pie as you add more advisors who are paid in equity.

Over time, the fictional founder in this graphic, “Ted,” ends up with only 25% equity in his company when he started with 100%.

It was our biggest mistake at KISSmetrics.

If you’re going to bring on advisors, make sure you negotiate their options well.

I’m not saying that you shouldn’t hire advisors.

The ones we had at KISSmetrics were very valuable, knowledgeable, and helpful.

Our only mistake was not paying attention to how fast we were diluting our own equity in the process.

You also need to make sure your advisors are contributing real value.

Many startup founders appreciate the connections their advisors have for introducing them to good talent or professional services, like lawyers, but your advisor isn’t just a Rolodex.

They should be providing long-term guidance and help with strategic decision-making.

Outsource wisely

In the early stages of your startup, you’re likely wearing a lot of hats.

From product design to HR and marketing, it starts with only you and your co-founder.

But as you grow, it’s important to know when to start outsourcing tasks that you no longer need to personally take care of.

Hiring a full team too soon can lead to negative cash flow, and soon enough, you’ll be laying everyone off and packing up your own desk.

Luckily, the Internet has provided countless ways to hire help for your startup.

Popular sites like Upwork, Freelancer, Fiverr, and People Per Hour allow you to connect with freelancers all over the world.

As I mentioned above, the freelance economy is booming.

You can find any type of freelancer you need on one of these platforms, from designers to marketers.

It may be tempting to outsource as soon as you have the money to do so.

I suggest waiting until you physically don’t have time to do the task anymore before outsourcing it.

This prevents you from spending money too soon, but it still lets you grow your startup when the time comes.

Thanks to these online platforms, finding a freelancer is quick and easy, so you don’t need a lot of notice.

Cut your expenses

If you haven’t already made a budget, do it.

You need to know what your fixed expenses are each month.

Fixed expenses are things like your rent, car payment, electric bill, and other things you can’t completely control.

You could sell your car, but you can’t make the electric company charge you any less.

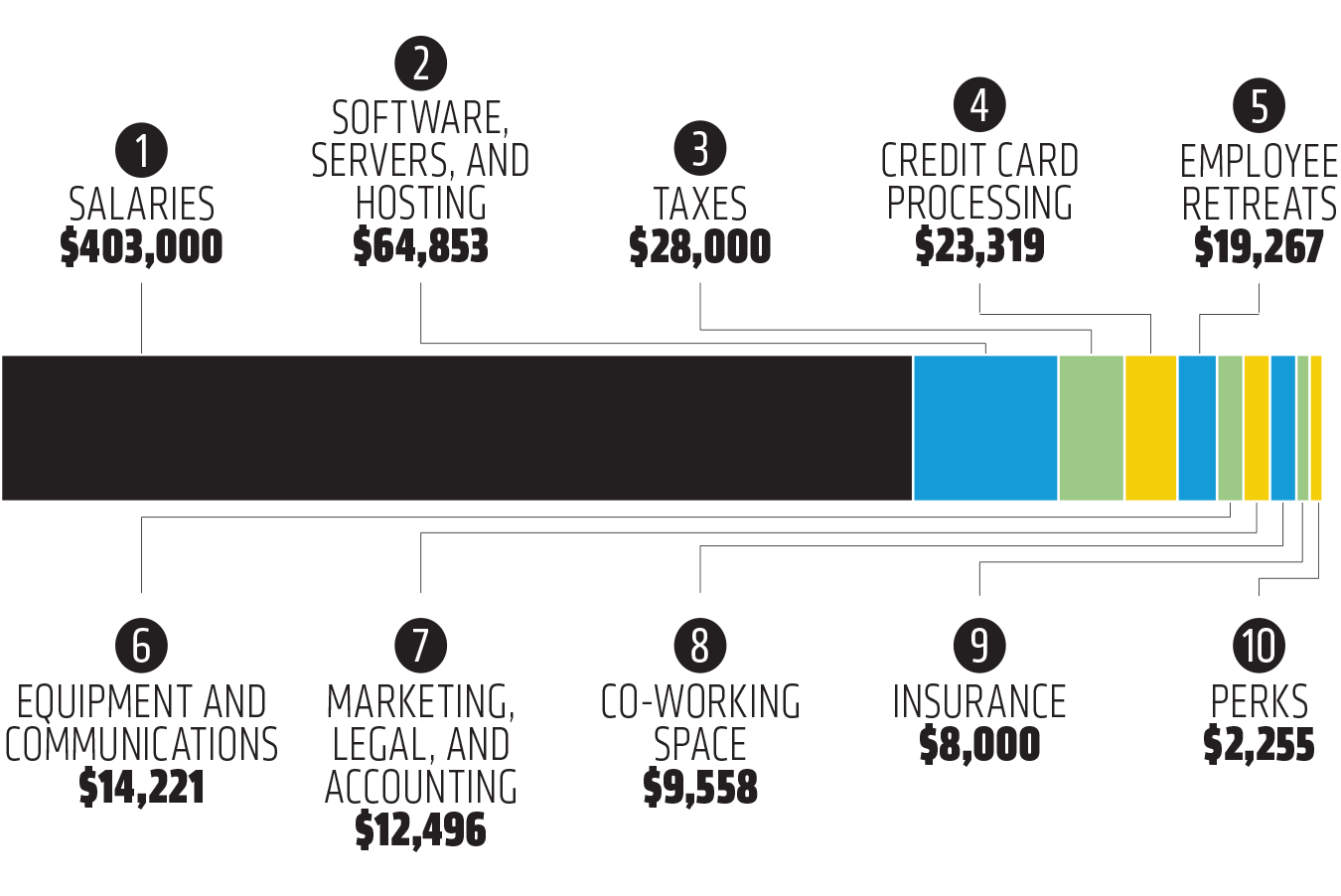

Social media scheduling company Buffer is notoriously transparent about their finances. Below is a representation of their monthly expenses.

Your startup won’t be spending anywhere near this amount yet. Buffer has over 70 employees and over 1 million customers.

When you’re starting out, you need to keep it lean.

A “lean startup” is actually a term Eric Ries came up with.

It means creating a startup that acts fast but also acts on data. That means conducting research about your customers and creating minimum viable products to test out that research.

It also means taking a pass on the expensive office space and big salaries many venture-funded startups have.

When Hiten and I were at KISSmetrics, we didn’t take a salary for a long time.

Eventually, after we received $10 million in venture funding, we decided to start paying ourselves. Our funders didn’t set a limit, so we limited ourselves to $5,000 per month each.

We were living in San Francisco at the time, so that wasn’t a lot of money with the city’s high rent and cost of living.

It’s important to realize that a startup isn’t a get-rich-quick scheme.

If you’re just in it for money, you won’t get very far. It takes years to build up the business to a point where you’ll likely be able to pay yourself a decent salary.

If you’re very lucky, years after that, you’ll grow even more to reach a multi-million dollar valuation.

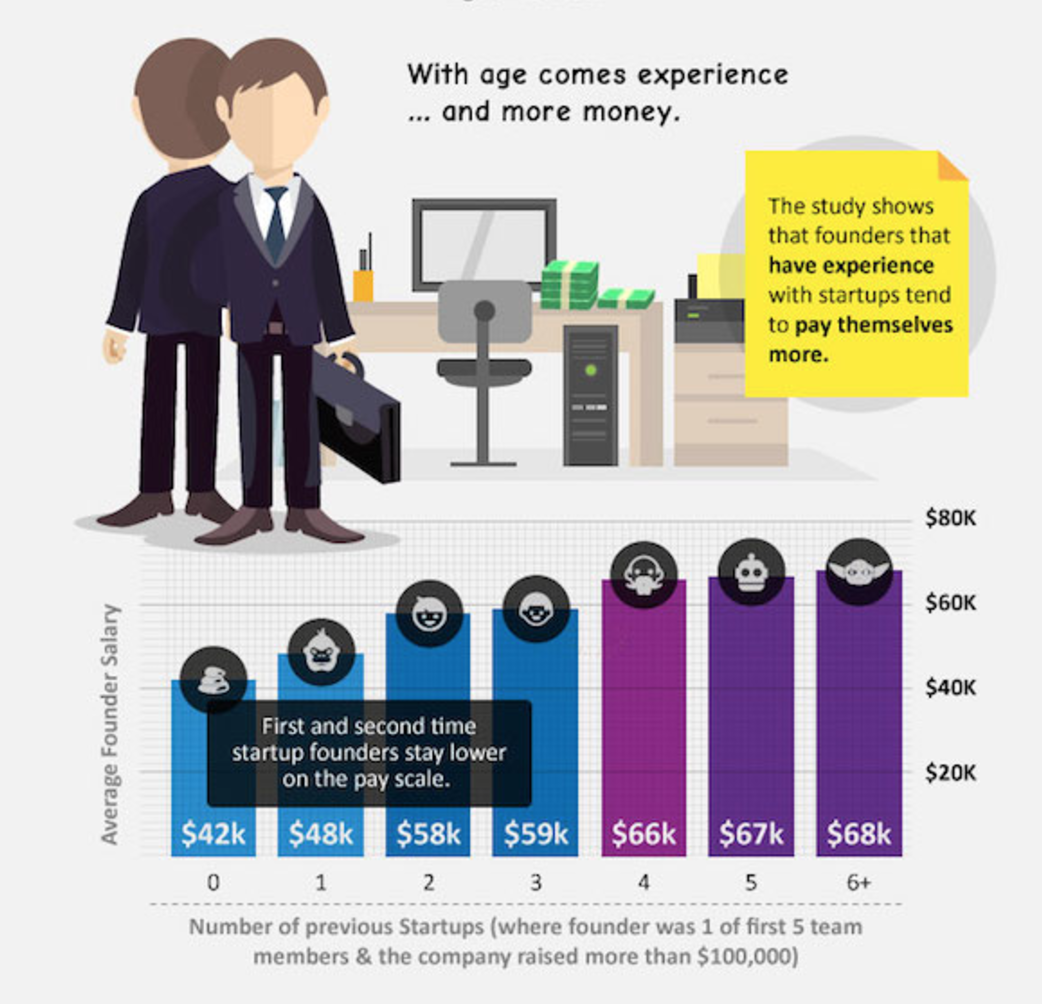

75% of startup founders are earning under $75,000 a year.

Repeat startup founders tended to pay themselves more. Even entrepreneurs who had previously started 6 or more businesses still paid themselves under $80,000 a year.

Depending on where you live, that’s either a lot of money or not very much.

Whatever your salary or budget is, get used to living frugally during the first few years of your startup.

I got used to not owning a car or wasting my money on things like games or the latest tech gadget.

I bought things that further my business and nothing else.

It may seem harsh, but that’s an entrepreneur’s reality — at least at first.

Invest in your brand

Okay, I’ve just told you to live frugally and not expect to have a lot of money, but now I’m saying that you should invest in branding.

Hear me out.

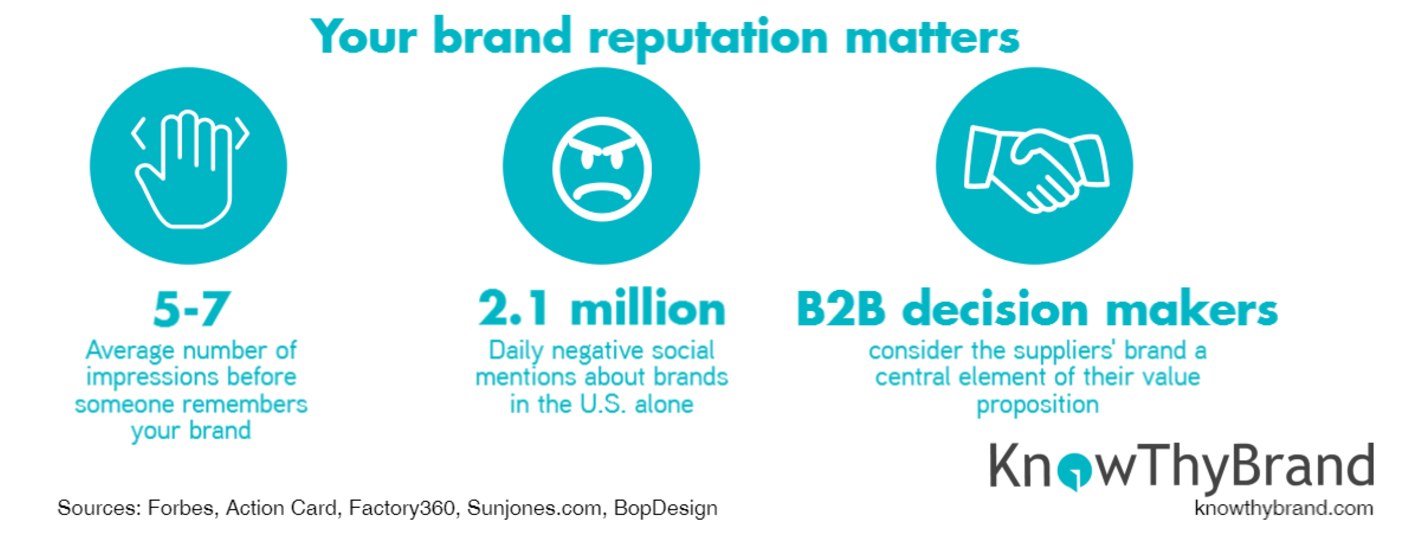

The value of a strong brand in today’s crowded marketplace is worth its weight in gold.

Your brand is what makes you different. It attracts new users and gets people’s attention among all the competition out there.

B2B decision-makers consider your brand an important factor when comparing suppliers.

I’ve written a lot about branding before. It’s so important for growing your business, especially to build user trust in the beginning.

It doesn’t need to cost a lot.

You can find freelance designers on the sites I mentioned earlier in this article, like Upwork.

Do a search for the elements you’ll need, like “logo design,” “website design,” or “email template design.”

You’re then taken to a results page of some of Upwork’s top logo designers.

Rates vary widely based on experience, location, and how many reviews a freelancer has. You can easily find someone in your budget here.

The really important part of investing in your brand is drawing in new users. With a strong brand promise, you can turn those users into brand advocates.

A brand advocate is a customer who is so passionate about your company that they willingly refer their friends and family to you.

They are powerful customers!

Referrals from brand advocates are 150x more likely to convert than regular leads.

Investing in your brand to create these loyal advocates is one of the smartest ways to spend your marketing budget.

Use content-marketing tactics to attract users

I’m going to recommend that you set up a content marketing strategy for your startup.

Big surprise, right?

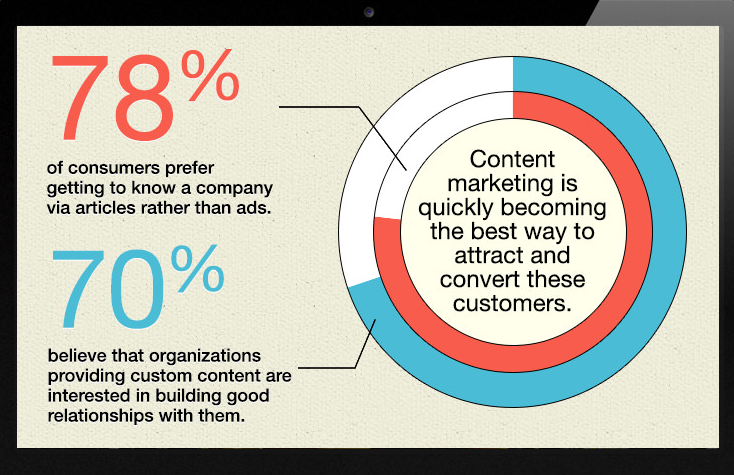

Content marketing is one of the most effective ways to reach new people. 70% of consumers think that brands who create original content want to build relationships.

You can either produce your own content or reach out to bloggers and other content creators.

When we were marketing Crazy Egg on a shoestring budget, we contacted all the top bloggers on Technorati.

We offered them our paid plan for free. Many of them ended up writing an article to review Crazy Egg.

This helped drive a lot of new users to us, and it didn’t take any effort beyond sending an email. The cost of giving away a few free accounts was easily made up in the users they referred.

One of the most powerful content marketing tools a startup can use is to create an explainer video.

This is a video that describes how your product works and what the key benefits are are in 30-60 seconds.

Think of it like a TV commercial for your startup.

Here’s an example of Mint’s explainer video:

We created an explainer video for Crazy Egg and instantly saw huge results.

Conversions went up 64%, which resulted in over $21,000 of new monthly revenue.

Video is increasingly popular among consumers. 92% of people who watch videos also share them with friends.

Using video in your marketing can grow your sales 49% faster.

Of course, blogging isn’t going out of style, either.

You’re reading this, aren’t you?

Whichever tactics you choose to make up your content marketing strategy, make sure you’re focusing on what your users want. Create content that answers their questions and objections.

A 2017 study by Time Inc found that 90% of consumers want custom content. So give it to them!

Conclusion

Bootstrapping your startup is hard work.

You need to raise enough money to form your company and work on your product in the first place. This often requires freelance or consulting work to pay the bills.

But you don’t need a lot of money to start a company.

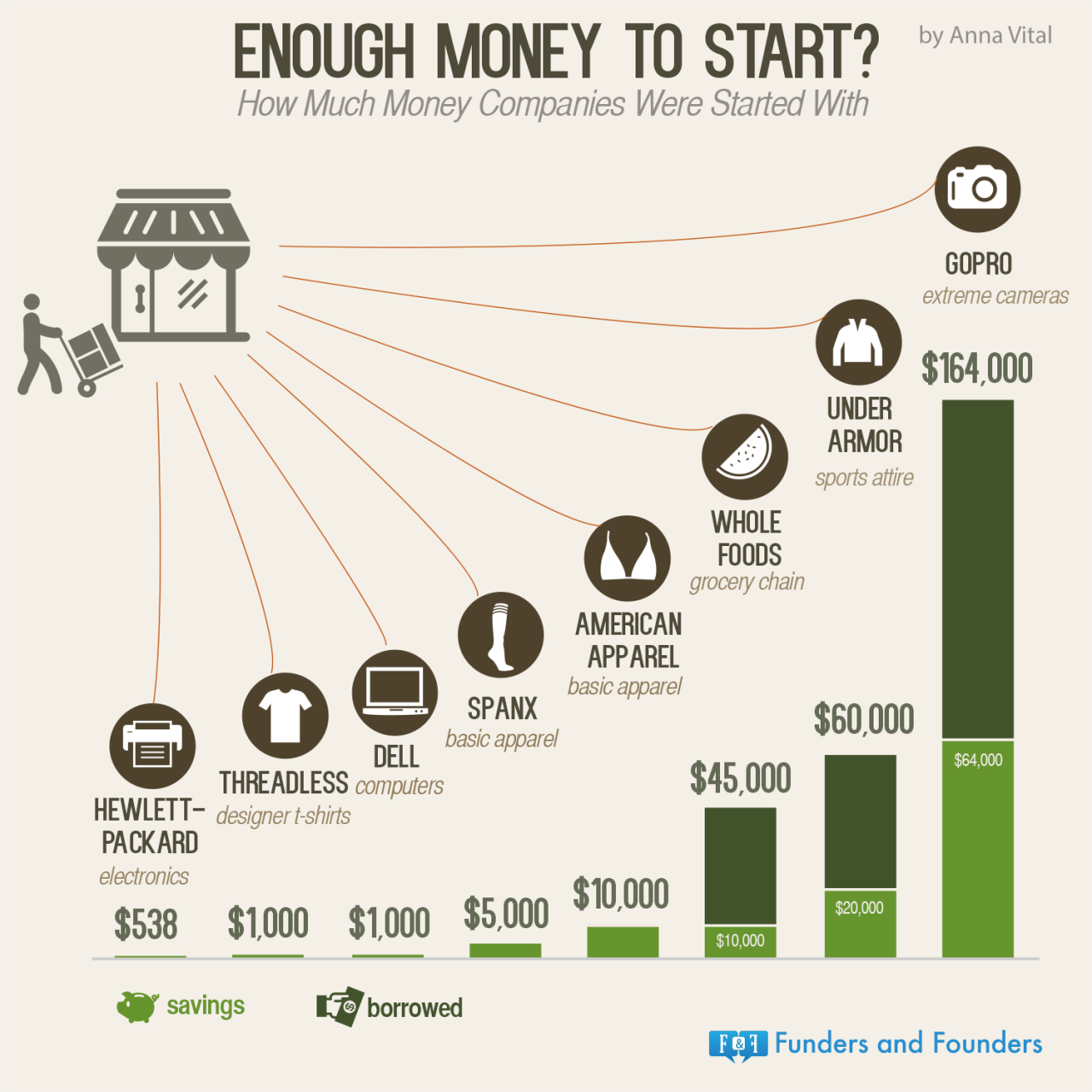

Some of the world’s most successful companies began with less than $10,000.

Hewlett-Packard was started with just $538 in a garage in Palo Alto, California!

That was a lot of money in 1936 when the company was founded, but that still equals only about $7,500 in today’s currency.

You need to find a compatible co-founder with skills that complement your own.

Or, you can go it alone, but being the only founder carries a lot of risk.

Seeking advice from seasoned pros is always a good idea, but it doesn’t come cheap. You’ll have to give up some equity.

You also need to learn when to do tasks yourself and when it’s time to outsource.

And while all this is going on, you need to maintain a strong brand presence and keep a watchful eye on expenses.

Oh yeah, and did I mention that you should tell anyone who will listen about your startup at networking events and in your blog and social media posts?

It’s really tiring.

I know because I’ve been there more than a few times.

Running your own successful startup is possible. I know that, too.

9 out of 10 businesses may eventually fail, according to statistics, but you can be that 1 success story if you keep trying.

Learning from failure will be your greatest strength.

Are you planning to start your own bootstrapped startup? Let me know in the comments!

Grow your traffic